Income tax - Accommodation work to accommodate age-related or disability-related loss of independence (tax credit)

Verified 17 April 2024 - Directorate for Legal and Administrative Information (Prime Minister)

Do you want to have equipment work done in your home for people with disabilities or seniors who are losing their independence? You can benefit, under conditions, from a tax credit. The rules change for expenses paid as of 2024. We'll tell you what you need to know.

Warning

For expenses paid since 1er january 2024, the tax credit is means-tested. It is reserved for people with intermediate incomes. If your income is modest or very modest, you must ask the new MaPrimeAdapt' premium. You cannot take advantage of both the tax credit and the new premium.

Expenditures paid in 2023

You must be resident for tax purposes in France and that housing must be your main dwelling.

You can be proprietor, tenant or occupant free of charge housing.

You must to have work carried out in your apartment.

The work must have been completed and invoiced before 31 december 2023.

Warning

the work must have been carried out by the same company.

You must have had work done in your home one of the following 2 categoriess:

- Work that facilitates access for the elderly or disabled

- Adaptation of the dwelling to loss of autonomy or disability, under conditions

Ouvrir l’image dans une nouvelle fenêtre

Silver

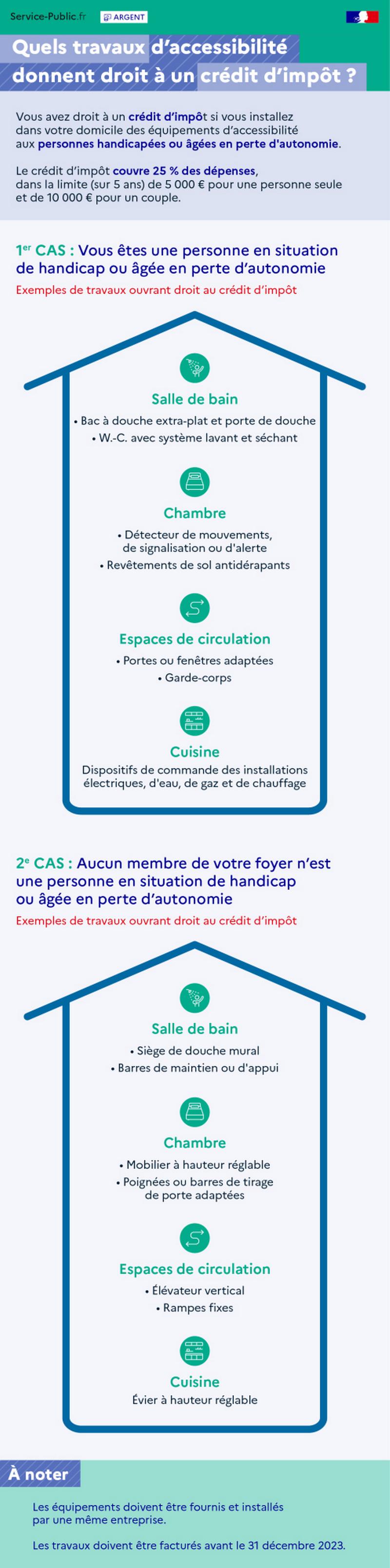

Which accessibility projects qualify for a tax credit?

You are entitled to a tax credit if you settle accessibility equipment in your home for disabled or elderly persons.

The tax credit covers 25% of expenses, up to a limit (over 5 years) of €5,000 for a single person and €10,000 for a couple.

1er case: You are a person with a disability or an elderly person who is losing independence (or you are responsible for it)

Examples of work eligible for the tax credit:

- Bathroom: extra-flat shower tray and shower door, toilet with washing and drying system

- Bedroom: motion, signaling or warning detector, non-slip floor coverings

- Traffic areas: adapted doors or windows, railings

- Kitchen: control devices for electrical, water, gas and heating installations

2e case: No member of your household is a person with a disability or an elderly person who is losing their independence

Examples of work eligible for the tax credit:

- Bathroom: wall shower seat, holding or support bars

- Bedroom: adjustable height furniture, adapted door handles or pull bars

- Traffic areas: vertical lift, fixed ramps

- Kitchen: adjustable height sink

Please note: equipment must be provided and settled by the same company. The work must be invoiced by December 31, 2023.

Répondez aux questions successives et les réponses s’afficheront automatiquement

Accommodation adaptation work

You or a member of your tax household must meet one of the following conditions :

- Accident at work Have a disability pension of at least 40% (military or for

- Have a mobility card inclusion (marked disability, priority or parking for disabled people)

- Suffer from a loss of autonomy giving entitlement to Custom Autonomy Allocation (APA)

Please note

If you are a parent of handicapped adult child, it can be considered to be at your expense and to be part of your tax household.

You can settle this equipment no matter what you are proprietor, tenant or free occupant.

Tax services consider as accessibility equipment (non-exhaustive list):

- Extra-flat shower tray and shower doors

- WC equipped with a washing and drying system

- Control system with motion, signaling or warning detector

- Electric roller shutters

- Non-slip flooring

- Sliding doors

- Adapted doors and windows

- Railing

- Closing, opening or control devices for electrical, water, gas and heating installations

Accessibility work

You can receive the tax credit even if no one in your household is a senior or a person with a disability (for example, to adapt your home in anticipation of a possible loss of independence).

You may have settled this equipment whether you own, rent or occupy for free.

Tax services consider as accessibility equipment (non-exhaustive list):

- Height-adjustable sink and washbasin

- Elevated toilet

- Holding or support bars

- Height adjustable furniture

- Adapted door handles or pull bars

- Vertical elevator apparatus and tilt elevator

- Stationary ramps

Tax credit rate

The rate is 25% of the amount of expenditure

Expenditure ceiling

Expenditure shall be limited to one of the following amounts :

- €5,000 for a single person

- €10,000 for a couple subject to common taxation

This ceiling shall be increased by €400 per dependent (€200 per child in alternate residence).

Warning

This ceiling shall be fixed for a period of 5 consecutive years. For example, for the year 2023, it relates to expenditures between the 1er January 2018 to December 31, 2023.

You must report the amount of expenses you paid in 2023 in the "Tax reductions and credits" of your statement.

Keep your expense documents because the tax authority can ask you for them (company invoice, vendor attestation).

If the amount of the tax credit exceeds the amount of tax owing, the excess will be returned to you.

Expenditures paid in 2024

The tax credit is now reserved for people with intermediate incomes, who meet certain conditions.

FYI

If your revenues are modest or very modest, you must apply for the new premium MaPrimeAdapt'. You cannot take advantage of both the tax credit and the new premium.

Accommodation

You must be resident for tax purposes in France and that housing must be your main dwelling.

You can own, rent or occupy the dwelling free of charge.

You must to have work done in your apartment.

The work must be completed and invoiced before 31 december 2025.

Warning

The work must be carried out by the same company.

Data subjects

You can only benefit from the tax credit if you are in one of the following 2 situations :

- Aged 60 years or older and with a loss of autonomy that places you in one of the groups 1 to 4 of the applicable national grid for the independent personality allowance

- With a disability rate equal to or greater than 50% (rate determined by decision of the CDAPH: titleContent)

You must also complete income conditions.

Your household income must be above the following income :

Number of persons in the household | Revenues Île-de-France | Revenues other regions |

|---|---|---|

1 | €27,343 | €20,805 |

2 | €40,130 | €30,427 |

3 | €48,197 | €36,591 |

4 | €56,277 | €42,748 |

5 | €64,380 | €48,930 |

Per additional person | €8,097 | €6,165 |

Please note

If your 2022 revenues are below or equal to these thresholds, your 2023 revenues are withheld.

Your revenues must also be below ceilings calculated based on the number of shares of your tax shelter.

The revenue limits are calculated as follows:

- €31,094 for 1re family quotient share

- €9,212 for each of the following 2 halves

- €6,909 for each additional half-share

Please note

If your 2022 revenues are greater than or equal to these limits, your 2023 revenues are deducted.

Example :

For a married or former couple, or 2 shares, resident in Île-de-France.

The minimum income to benefit from the tax credit is €40,130.

The income not to be exceeded shall be: €31,094 + (€9,212 x2) = €49,518

You must have carried out in your accommodation housing adaptation works loss of independence or disability.

You must have settled one or more pieces of equipment in your accommodation in the following categories:

- Sanitary facilities

- Safety and accessibility equipment

The equipment concerned is as follows:

Répondez aux questions successives et les réponses s’afficheront automatiquement

Sanitary facilities

- Height-adjustable sink and washbasin

- Fixed sink and washbasin for use by a person with reduced mobility

- Offset Siphon

- Wall-mounted shower seat

- Full shower cubicle for persons with reduced mobility

- Extra-flat shower tray and shower door

- Tiled shower tray

- Lifting pump or water suction pump for extra-flat receiver

- Elevated W-C

- Hanging toilet with support frame

- Toilet equipped with washing and drying system

- Taps for persons with reduced mobility

- Thermostatic mixer

- Tilting mirror for persons with reduced mobility

Attached safety and accessibility equipment

- Holding or support bar

- Handrail

- System for motorizing shutters, entrance and garage doors and gates

- Electric roller shutter

- Control system comprising a movement, signaling or warning detector

- Device for closing, opening or control of electrical, water, gas and heating installations

- Timed lighting coupled to a motion sensor

- Adapted door handle or pull bar

- Indwelling transfer system or ceiling bracket

- Fixed ramp

- Inclined plane

- Height adjustable furniture

- Podotactile coating

- Contrasting and non-slip gait nose

- Non-slip flooring

- Angle protection

- Railing

- Adapted door or window

- Door reversal or widening

- Sliding door

- Magnetic loop

- Vertical lift apparatus comprising a platform arranged for transporting a disabled person and a tilted lift especially designed for transporting a disabled person

Tax credit rate

The rate is 25% of the amount of expenditure

Expenditure ceiling

Expenditure shall be limited to one of the following amounts:

- €5,000 for a single person

- €10,000 for a couple subject to common taxation

This ceiling shall be increased by €400 per dependent (€200 per child in alternate residence).

Warning

this ceiling shall be fixed for a period of 5 consecutive years. For example, for the year 2024, it relates to expenditures between the 1er January 2019 to December 31, 2024.

You will declare in 2025 your expenses paid in 2024.

Keep your expense documents because the tax authority can ask you for them (company invoice, vendor attestation).

If the amount of the tax credit exceeds the amount of tax owing, the excess will be returned to you.

Who can help me?

Find who can answer your questions in your region

For general information

Tax Information Service

By telephone:

0809 401 401

Monday to Friday from 8:30 am to 7 pm, excluding public holidays.

Free service + call price

To contact the local service managing your folder

Department in charge of taxes (treasury, tax department...)

Tax credit for expenditure on aid to persons (Article 200c(A))

List of equipment specially designed for the elderly or disabled (Article 18b)

FAQ

Service-Public.fr

Service-Public.fr

Ministry of Finance

Ministry of Finance

Ministry of Finance

Ministry of Finance

National Housing Agency (Anah)