Tax scale What is the income tax?

Verified 06 June 2024 - Directorate for Legal and Administrative Information (Prime Minister)

The scale is used for calculating your tax.

He is progressive. It includes multiple income brackets, which each correspond to a different tax rate, which varies from 0% to 45%.

Tax scale To apply the previous tax to your taxable income, you must take into account the family quotient, that is, your number of shares, which depends on your situation and the number of people in your tax household.

Please note

Tax scale The processor is fixed every year. For example, the 2024 scale (applicable to 2023 income) is set by the 2024 budget.

Income brackets | Income tax bracket rate |

|---|---|

Up to €11,294 | 0% |

From €11,295 to €28,797 | 11% |

From €28,798 to €82,341 | 30% |

From €82,342 to €177,106 | 41% |

More than €177,106 | 45% |

The marginal tax rate (TMI) is the tax rate that applies to the highest tranche of your income.

The average tax rate is the average rate at which your income is taxed. It tells you the how much your tax represents in your income.

Please note

The child tax benefit is limited. It's the family quotient ceiling.

Here are some examples of the calculations:

Répondez aux questions successives et les réponses s’afficheront automatiquement

For a single man

One unmarried (household of a single share) whose net taxable income is €30,000, without any reduction or deduction.

His family quotient is €30,000.

For the calculation of his tax:

- Up to €11,294 : 0%

- From €11,295 to €28,797 : (€28,797 - €11,294) × 11% = €17,503 × 11% = €1,925.33

- From €28,798 to €30,000 : (€30,000 - €28,797) x 30% = €1,203 × 30% = €360.90

Its gross tax is: €0 + €1,925.33 + €360.90 = €2,286.23.

The marginal tax rate (BIT) of this taxpayer is 30%, because its family quotient puts it in that range. But not all his income is taxed to 30%.

For a married couple or a past couple without children

Taxable net income of €60,000

One married couple or former couple without children (household of 2 units) having received taxable net income of €60,000.

His family quotient is €60,000 : 2 = €30,000.

For the calculation of his tax:

- Up to €11,294 : 0%

- From €11,295 to €28,797 : (€28,797 - €11,294) × 11% = €17,503 × 11% = €1,925.33

- From €28,798 to €30,000 : (€30,000 - €28,797) x 30% = €1,203 × 30% = €360.90

The gross tax for each member of the couple is: €0 + €1,925.33 + €360.90 = €2,286.23.

This tax must be multiplied by the number of shares in the tax household. In this example, it will be multiplied by 2 since it is a married or a former couple.

The couple will therefore have to pay a tax of €2,286.23 × 2, or €4,572.46.

The marginal tax rate (IMR.) for this couple is 30%, because its family quotient puts it in that range. But not all his income is taxed to 30%.

Taxable net income of €90,000

One married couple or former couple without children (household of 2 units) having received taxable net income of €90,000.

His family quotient is €90,000 : 2 = €45,000.

For the calculation of his tax:

- Up to €11,294 : 0%

- From €11,295 to €28,797 : (€28,797 - €11,294) × 11% = €17,503 × 11% = €1,925.33

- From €28,798 to €45,000 : (€45,000 - €28,797) x 30% = €16,203 × 30% = €4,860.90

The gross tax for each member of the couple is: €0 + €1,925.33 + €4,860.90 = €6,786.23.

This tax must be multiplied by the number of shares in the tax household. In this example, it will be multiplied by 2 since it is a married or a former couple.

The couple will therefore have to pay a tax of €6,786.23 × 2, or €13,572.46.

The marginal tax rate (IMR.) for this couple is 30%, because its family quotient puts it in that range. But not all his income is taxed to 30%.

For a married or spent couple with 2 children

Taxable net income of €60,000

One married or past couple with 2 children (focus of 3 shares, 1 share for each parent and 1 half share for each child) who received net taxable income of €60,000.

His family quotient is €60,000 : 3 = €20,000.

For the calculation of his tax:

- Up to €11,294 : 0%

- From €11,295 to €20,000 : (€20,000 - €11,294) x 11% = €8,706× 11% = €957.66

This tax must be multiplied by the number of shares in the tax household. In this example, it will be multiplied by 3 since it is a married or past couple with 2 children.

The couple with 2 children should therefore pay a tax of: €957.66 x 3, or €2,872.98

The couple shall be entitled to a maximum tax advantage of €3,518 (€1,759 x 2) for his 2 children (it is the family quotient ceiling).

A married or non-married couple who have received a net taxable income of €60,000 will have to pay a tax of €4,572.46.

The advantage associated with the 2 children is therefore €1,699.48 (€4,572.46 - €2,872.98).

The amount of this benefit shall be less than the maximum benefit of €3,518.

The couple with 2 children will therefore have to pay a tax of €2,872.98

The marginal tax rate (BIT) for this couple with 2 children is 11%, because its family quotient puts it in that range. But not all his income is taxed to 11%.

Taxable net income of €90,000

One married or past couple with 2 children (focus of 3 shares, 1 share for each parent and 1 half share for each child) who received net taxable income of €90,000.

His family quotient is €90,000 : 3 = €30,000.

For the calculation of his tax:

- Up to €11,294 : 0%

- From €11,295 to €28,797 : (€28,797 - €11,294) × 11% = €17,503 × 11% = €1,925.33

- From €28,798 to €30,000 : (€30,000 - €28,797) x 30% = €1,203 × 30% = €360.90

The gross tax for each member of the couple is: €0 + €1,925.33 + €360.90 = €2,286.23.

This tax must be multiplied by the number of shares in the tax household. In this example, it will be multiplied by 3 since it is a married or past couple with 2 children.

The couple with 2 children should therefore pay a tax of €2,286.23 × 3, or €6,858.69.

The couple shall be entitled to a maximum tax advantage of €3,518 (€1,759 x 2) for his 2 children (it is the family quotient ceiling).

A married or non-married couple who have received a net taxable income of €90,000 will have to pay a tax of €13,572.46.

The advantage related to children is €6,713.77 (€13,572.46 - €6,858.69).

This amount exceeds the maximum tax benefit to which the couple is entitled for their 2 children of €3,195.77 (€6,713.77 - €3,518).

The couple with 2 children will therefore have to pay a tax of €10,054.46 (€6,858.69 + €3,195.77).

The marginal tax rate (BIT) for this couple with 2 children is 30%, because its family quotient puts it in that range. But not all his income is taxed to 30%.

For a single parent with 2 children

One single parent with 2 children (household of 2.5 shares, 1 share for the parent, 1 half share for each child in principal residence and 1 additional half share as a lone parent) who received taxable net income of €30,000.

His family quotient is €30,000 : 2.5 = €12,000.

- Up to €11,294 : 0%

- From €11,295 to €12,000 : (€12,000 - €11,294) x 11% = €706 x 11% = €77.66

This tax must be multiplied by the number of shares in the tax household. In this example, it will be multiplied by 2.5 since it is a lone parent with 2 children.

Please note : the tax benefit is divided by two in the case of alternate residence.

The gross tax of the family is: €77.66 x 2.5, or €194.15.

The marginal tax rate (BIT) for this family is 11%, because its family quotient puts it in that range. But not all his income is taxed to 11%.

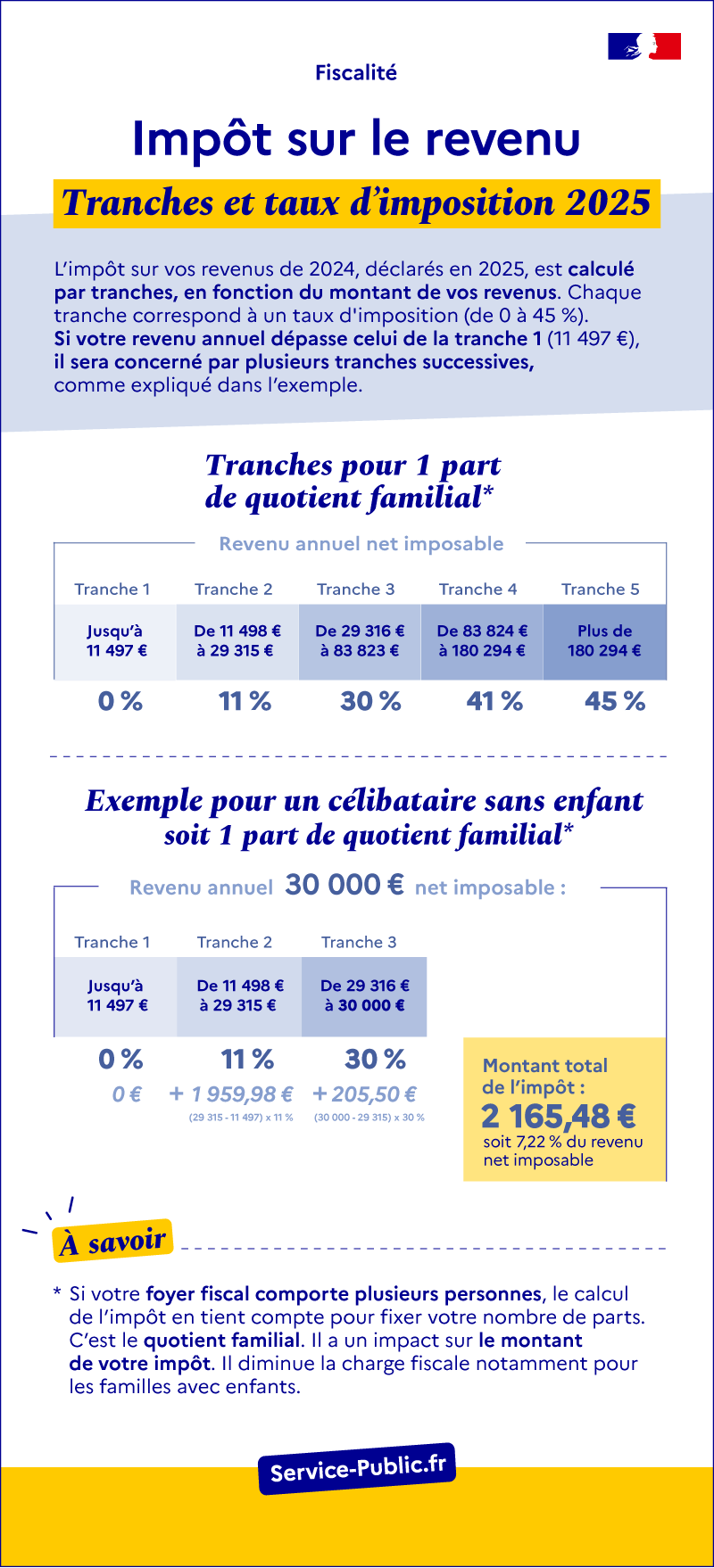

Infographie - Income tax: 2024 schedule

Ouvrir l’image dans une nouvelle fenêtre

Income tax

2024 tax brackets and rates

Your tax is calculated in installments, based on the amount of your income. Each bracket corresponds to a tax rate (from 0 to 45%). If your annual income exceeds that of bracket 1 (€10,777), it will be covered by several successive brackets, as explained in the example.

Slices for 1 share of family quotient:

- Up to €11,294 (bracket 1): 0% tax rate

- From €11,295 to €28,797 (bracket 2): tax rate of 11%

- From € 28 798 to € 82 341 (bracket 3): 30% tax rate

- From €82 342 to €177 106 (bracket 4): tax rate of 41%

- More than €177 106 (bracket 5): tax rate of 45%

Example of calculation for 1 share of family quotient:

A single person (1 share) whose annual net taxable income is €30,000, the calculation of his tax is as follows:

- Up to €11,294 (tranche 1): €0

- From €11 295 to €28 797 (tranche 2): €1 925.33

- From €28 798 to €30 000 (tranche 3): €360.90

Total tax: €2,286.23, or 7.62% of his net taxable income.

That is, if you have more than one person in your tax household, the tax calculation takes that into account when determining your number of shares. This is the family quotient. This mechanism has an impact on the amount of your tax. In particular, it reduces the tax burden for families with children.

Warning

the scale is only one element of the calculation of income tax. You can estimate your tax liability using the Tax Services Simulator.

Who can help me?

Find who can answer your questions in your region

For general information

Tax Information Service

By telephone:

0809 401 401

Monday to Friday from 8:30 am to 7 pm, excluding public holidays.

Free service + call price

To contact the local service managing your folder

Department in charge of taxes (treasury, tax department...)

Calculation of income tax

Amount below which the tax is not assessed (Article 1657)

Online service

Online service

Simulator

FAQ

Service-Public.fr

Ministry of Finance

Ministry of Finance